Financial Planning 101

Many young persons may view planning for retirement as something to consider when they're closer to their middle ages, or when they have the "dream job" or have "settled down." This is a common mistake that will cost you YEARS of potential investment returns that you will NEVER get back.

When planning for the future, time is by and large the most valuable asset at one's disposal. Organizing your finances as a youthful individual is also incredibly simple, and can be done yourself.

Make sure that your financial "house" is in order before devising a plan to save and invest your cash to fund your future goals. As a young person, there are not many hoops to jump through, but there are certain items to address in order to prevent a financial catastrophe and to ensure you maximize your money's potential.

Financial Priorities

| Priority | Details |

|---|---|

| 1. Stable Income | This may seem obvious, but it is a requirement in order to meet many of the other necessities below. |

| 2. Establish Emergency Fund | Set aside 3-months of living expenses in a safe place (checking/savings, low-risk investments, etc.). |

| 3. “Bad Debt” Free | Credit cards, car payments, other debt with a high interest rate (>7%). |

| 4. Invest! |

|

| 5. Insurance Coverage |

Insure properly:

|

Investment Accounts

The most common type of investment accounts available to the average investor includes Employer-sponsored plans (401k, 403b, etc.), Individual Retirement Accounts (Roth IRA, Traditional IRA, etc.), and investment accounts (Non-retirement accounts).

Employer-sponsored Retirement plans

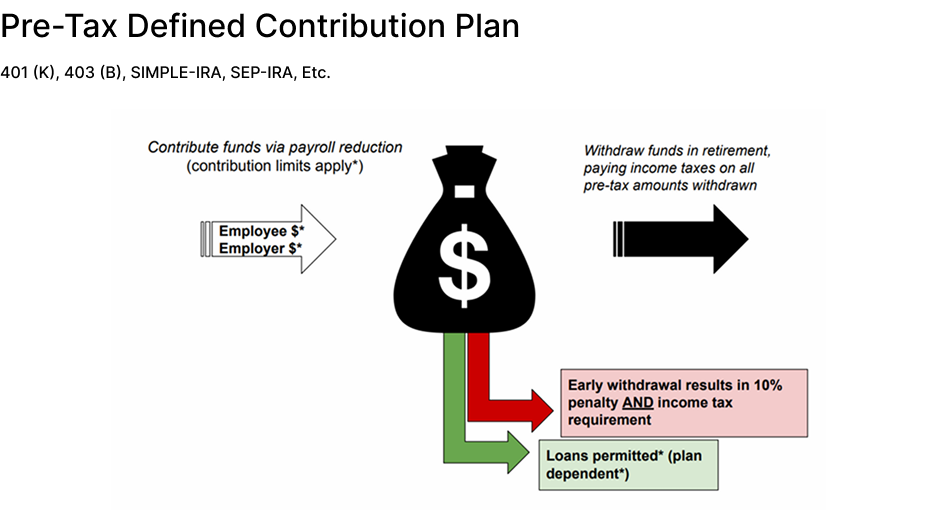

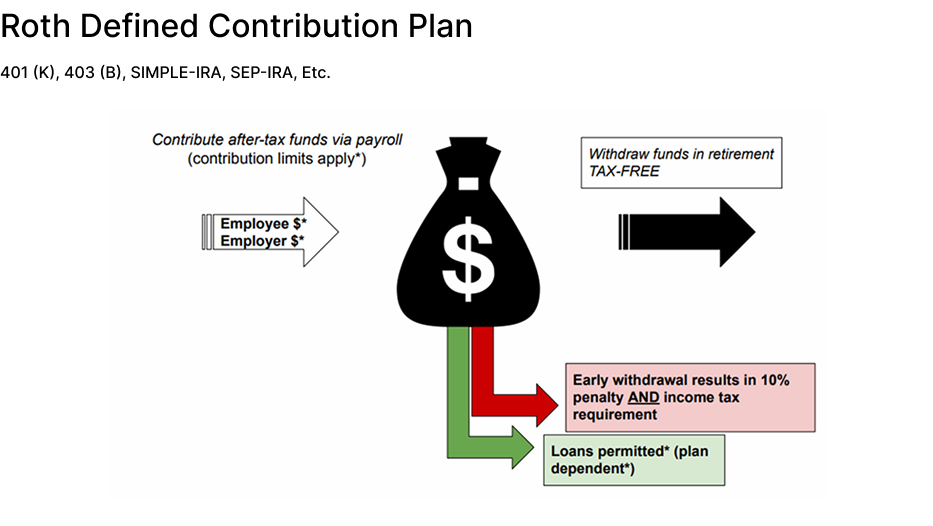

Employer-sponsored Retirement plans: These plans are the most commonly available to US employees by and large. Defined contribution plans are predominantly Pre-tax/Traditional (monies taxed when withdrawn, ideally in retirement) or After-tax/Roth (monies taxed now, growing tax-free for your lifetime) and allow for employees to contribute a maximum of $24,500 (2026) each year, along with the employer being able (though may not be required) to contribute a percentage of an employee's salary into the account.

How does one "invest" in their employer-sponsored plan? This depends on the custodian your employer has elected to oversee employee accounts. I stress the word "oversee" as it is purely the responsibility of the employee to manage their own investments in the account, the plan provider is simply the custodian of employee accounts.

Many employers will use Vanguard, Fidelity, Charles Schwab, and others to custody their company's plan. Depending on how much your employer is willing to spend, a predetermined list of investments will be available to choose from ("investment options").

The information discussed above is more than enough for most people to be aware of, but the details can be viewed in greater depth here.

Individual Retirement Accounts (IRAs)

Individual Retirement Accounts (IRAs):

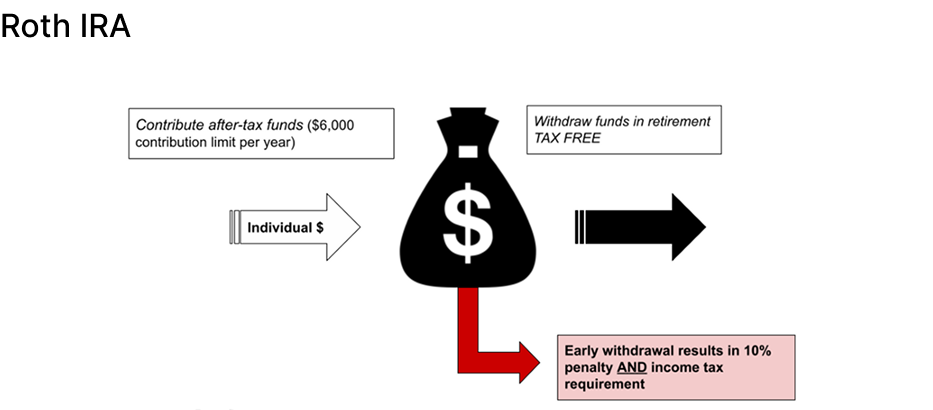

IRAs (Traditional or Roth): Individual Retirement Accounts are self-funded retirement accounts, with no affiliation to an employer-sponsored account. IRAs are individual, meaning they are not "joint" accounts owned by two or more persons. All that is required in order to contribute funds to an IRA is to have "earned income." If single, you must earn an equal amount of taxable income that is contributed, spouses may contribute for each other if one is not working. Certain income amounts will phase out an individual or couple from contributing to an IRA, view the details here.

Roth IRA (The tax-free individual retirement account): Roths are arguably the most efficient retirement account that an individual can contribute to, especially a young person. This is primarily due to benefitting from decades of tax-free compounding growth inside an investment account.

As an individual naturally progresses in their career, so will their income and as a result, the rate at which they will be expected to pay taxes. The key to a Roth is to invest as much as possible into the account until the IRS no longer allows direct contributions, which is when a single person's income crosses over $153,000 (2026) or a married couple surpasses $242,000 of income. There are strategies to side-step this income limitation.

Benefits:

- The investment earnings in the account can be withdrawn completely tax free* in retirement (age 59 ½).

- Years of compounding interest on investment earnings.

- The Roth IRA can double as a "catastrophe fund," allowing for penalty-free withdrawals in the case of death, disability, unpaid medical expenses, and more.

Taxable Investment Accounts

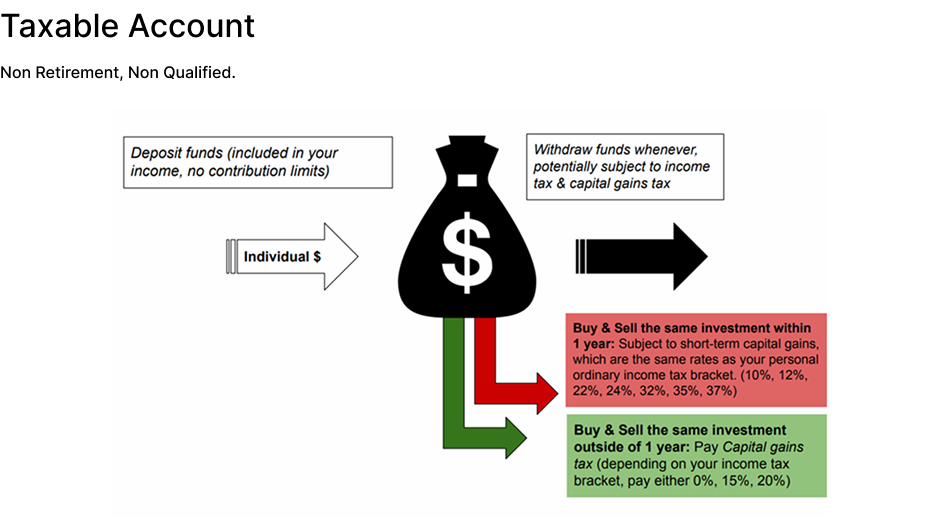

Taxable Investment Accounts: Some of the most notable benefits associated with these accounts are that no maximum annual contribution applies, no withdrawal penalties do either, and they can be jointly owned by 2 or more persons. The IRS allows this to take place as they will be able to collect taxes on profits gained in the account.

There are limited tax-shelter benefits offered as opposed to those available with retirement accounts. The taxation of an investment account is slightly more complicated than is the case with retirement accounts, but it is still relatively straightforward. No tax is owed from the account until a "gain" occurs (or is realized) in excess of the amount originally invested. This "gain" can take on a few different forms, such as a capital gain, dividend, or distribution.

Capital Gains: Not all gains are created equal

-

Short-term Capital Gains: An investment is bought and sold (realized) within 1-year (<365 days). The gain on the investment will be taxed at the income tax rate the individual is subject to.

For example, if a single share of Microsoft (MSFT) is purchased at $220 and sold within 1-year for $300, taxes owed on that share of stock amount to the $80 gain multiplied by the owner’s corresponding ordinary income tax rate.

-

Long-term Capital Gains: An investment is bought and sold (realized) outside of 1-year (>365 days). The gain on the investment will be taxed at the capital gains tax rate the individual is subject to. This is a separate bracket altogether from income tax rates, and the rates are much more favorable. This is the government's way of encouraging longer-term stock ownership, rather than gambling with the stock market (day trading).

For example, if a single share of Microsoft (MSFT) is purchased at $220 and sold outside of 1-year for $300, taxes owed on that share of stock amount to the $80 gain multiplied by the owner’s corresponding capital gains tax rate.

Income: Income generated within a taxable account is also subject to tax, this may be in the form of a dividend, distribution, or interest.

- Dividends: Dividends are paid to shareholders as determined by a company’s board of directors. Dividends received from a US-based company are deemed “Qualified” and are subject to capital gains rates for taxation reasons, while foreign companies pay out “Non-Qualified” dividends and are subject to ordinary income tax rates.

- Distributions: These are cash payments received from an investment, typically paid out by a Mutual fund as a result of a sale taking place within the fund. The distribution will be characterized as a short-term (ordinary income) or a long-term (capital gains) distribution, depending on how long the securities were held.

- Interest: Income received from a checking/savings account, CD, or bond, is subject to ordinary income tax rates.

Which accounts should you utilize to fund your goals?

Short-term goals (house down payment, emergency fund, additional savings, etc.):

- Utilizing a taxable investment account may be your best bet. Withdrawing funds from a retirement account is not preferable as these funds are best used to capitalize on long-term growth for retirement, premature withdrawals will stunt their growth.

- In certain situations, a loan from your 401(k) may be an option to consider. Each plan will vary in its rules and regulations in allowing withdrawals, and should only be considered for smart purchases that will help grow your net worth (buying a house may be a good idea, but buying a car is likely NOT). Keep in mind a loan from your 401(k) is required to be paid with interest to avoid penalties, but the interest will essentially be used to pay yourself back. Ideally, loans from a retirement plan should probably be avoided.

Long-term goals:

- Tax-advantaged accounts are probably the best option to consider when planning for your long-term goals, which should include planning for retirement. The more you save, the more likely you are to accumulate wealth tax-efficiently and fund your financial independence.